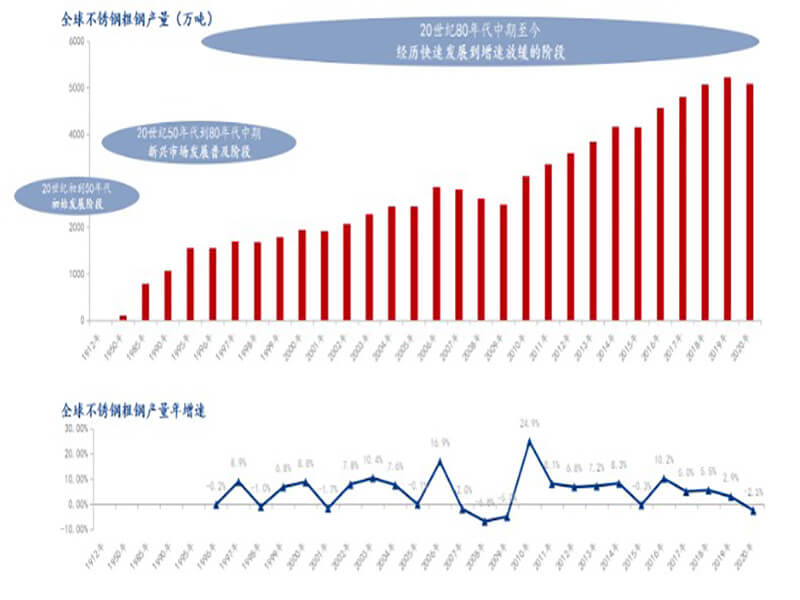

The development of the global stainless steel industry has gone through hundreds of years and has gone through about three stages:

Germany, Britain, the United States, and other countries have developed martensitic, ferritic, and austenitic stainless steels almost simultaneously. After about 40 years of development, the global stainless steel output was about 1 million tons in the early 1950s. At this stage, the application of stainless steel is mainly in some areas with special requirements for corrosion resistance and high-temperature resistance.

Entering 1950, the American stainless steel industry took the lead in realizing civilian use, and stainless steel production gradually realized accelerated development. After another 40 years of development, by 1990, the global stainless steel production exceeded 10 million tons. During this period, stainless steel smelting technology, continuous casting technology and multi-roll cold rolling mill technology represented by out-of-furnace refining were successfully developed, which promoted the large-scale development of global stainless steel. At this stage, stainless steel began to enter the homes of common people, and the level of civilian use began to gradually expand.

1990-2000 market expansion period; 2000-2016 accelerated development stage; 2016 to present, growth slowdown stage

Since the 1990s, the development of the stainless steel industry has broken through traditional markets such as Europe, America, and Japan, and has begun to develop into broader emerging markets. The first large-scale main production area in the history of the global stainless steel industry was born in the 1990s, namely the European stainless steel market. After more than ten years of development, by 2002, the global stainless steel output exceeded 20 million tons.

Entering the 21st century, the global stainless steel industry has further accelerated its development. The production and consumption of stainless steel in developing countries continue to grow, especially the rapid economic development of China and other countries in the Asia-Pacific region, as well as the increase in consumption in the civilian sector, which has driven the rapid growth of global stainless steel production. However, during the global financial crisis in 2008, there was a negative growth in stainless steel production for two years. From 2010 to 2016, the global crude steel production growth rate maintained double-digit growth, and China played a leading role.

Since 2017, the growth rate has slowed year by year. In 2019, the global stainless steel crude steel production reached 52.218 million tons, but the annual growth rate slowed to 2.94%. The global spread of the new crown epidemic in 2020 has brought huge challenges to the normal operation of the stainless steel industry. Global stainless steel crude steel production fell to 50.892 million tons, a decrease of 2.5% year on year.

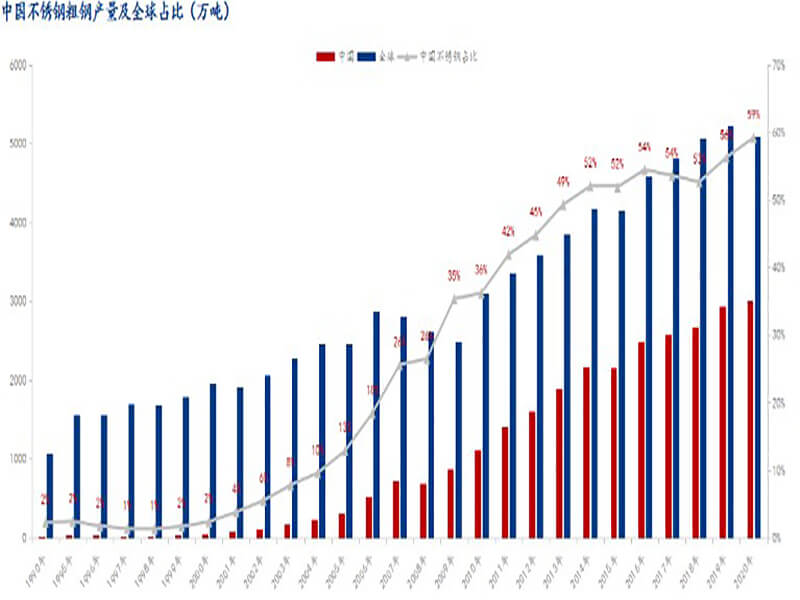

The development of Chinese stainless steel has roughly gone through four stages:

Our country has established some special steel enterprises mainly through learning from the Soviet Union. At this stage, the demand for stainless steel is mainly for cutting-edge use in industry and national defense, and the annual output of stainless steel is very small.

The focus of national work has shifted to modernization. By 1999, apparent consumption had increased significantly to 1.53 million tons, and output was only 300,000 tons.

With the rapid development of the national economy and the continuous improvement of people’s living standards, the demand for stainless steel is growing rapidly, and the large-scale use of domestic nickel pig iron has greatly reduced the cost of stainless steel in China. At this stage, the apparent consumption of stainless steel exceeded 5 million tons and reached more than 6.5 million tons in 2007

Since April, the price of stainless steel charge has dropped significantly, and the cost of stainless steel has dropped rapidly. In March, although domestic stainless steel profits were average, steel mills were still enthusiastic about production. The output of stainless steel crude steel reached 3.03 million tons, of which the output of 300 series reached 1.38 million tons. Entering April, the profit of stainless steel was significantly restored because of the rapid decline in the price of charge at the raw material end. From the perspective of production scheduling, the start of stainless steel still remains at a high level, with few overhauls, production levels flat from the previous month, and sufficient supply. The agency predicts that as the demand for the stainless steel market picks up in the future, the price of stainless steel is inevitable.

According to a news from the Ministry of Finance website on July 29, in order to promote the transformation and upgrading and high-quality development of the steel industry, with the approval of the State Council, the State Council’s Tariff Commission issued an announcement that from August 1, 2021, the Export tariffs will be adjusted to 40% and 20% export tariffs. This policy mainly involves some 23 types of steel products including cold-rolled coils, electro-galvanized sheets, tin-plated sheets, silicon electrical steel, and petroleum pipes. The policy adjustments are still aimed at reducing domestic steel exports, ensuring the supply of domestic steel resources, and supporting the country. The implementation of policies to reduce crude steel output, guide the steel industry to reduce total energy consumption, and promote the transformation and upgrading of the steel industry and high-quality development.

For Further Details,Please Feel Free To Contact Us: